If you feel like everyone is talking about crypto and you are quietly nodding along, this is for you.

Cryptocurrencies are digital assets , like Bitcoin and Ethereum, that live on open networks and use cryptography and blockchain instead of banks or governments to record and verify transactions. No coins to hold, no paper notes, just code and a big shared database.

Before we go deeper, quick but important note. Nothing here is financial, tax, or legal advice. Crypto is high risk. You can lose some or all of your money. My aim here is to help you actually understand what you are doing before you click “buy”.

Cryptocurrencies, explained

Let's strip it right back.

A cryptocurrency is:

- Fully digital, there is no physical coin or note

- Not issued by a central bank, instead it runs on a network of computers around the world

- Recorded on a public database called a blockchain, where anyone can see transactions

You can think of a blockchain as a shared spreadsheet that lots of people copy and update, where every change is checked and agreed by the network.

You will hear a few related terms, and they do matter:

- Cryptocurrency usually means a coin like Bitcoin or Ether that can be used in payments or as an investment

- Cryptoasset is broader, it includes coins, tokens, stablecoins, NFTs and so on

- Digital asset is broader again, it can include tokenized bonds, tokenized deposits, and other financial products sitting on a blockchain

Coins vs tokens vs general “digital currency”

This part confuses almost everyone at first, so if you are unsure, you are not alone.

Coins A coin is native to its own blockchain.

- Bitcoin (BTC) lives on the Bitcoin network

- Ether (ETH) lives on the Ethereum network

- SOL lives on Solana

The coin is built into the base protocol. It is used to pay transaction fees and sometimes for securing the network.

Tokens Tokens are created on top of an existing blockchain.

On Ethereum, for example, you have:

- ERC-20 tokens like USDT, USDC, many DeFi tokens

- Governance tokens for protocols

- In-game tokens, loyalty tokens, and so on

The easiest way to think about it is this. The coin is like the fuel of the network. Tokens are like apps or tickets that run on top of that network.

Digital currency This is a broad phrase people throw around:

- It can include cryptocurrencies

- Stablecoins

- Central bank digital currencies (CBDCs)

- Tokenized bank deposits

And here is a key point for you as an everyday user. The “digital money” you see in your banking app is not a cryptocurrency. It is just a digital record of your regular bank balance, controlled entirely by your bank and the local banking system.

Brief history, from Bitcoin to today

A quick bit of history helps you understand the mindset behind crypto.

- In 2008, during the global financial crisis, someone using the name Satoshi Nakamoto published the Bitcoin whitepaper

- In 2009, the Bitcoin network launched, with the idea of “peer-to-peer electronic cash”, so people could send value directly without a bank

- Early years were experimental, small communities mining coins on home computers

Then things moved fast:

- Ethereum launched, bringing smart contracts, which let you program money and build applications directly on the blockchain

- Thousands of “altcoins” appeared, some serious, lots of junk

- Stablecoins grew as a way to park value in dollars while staying inside the crypto ecosystem

- DeFi, NFTs, memecoins, gaming tokens, all exploded in waves

- The whole space went from obscure technology to a multi-trillion dollar asset class, then back down, then up again

So if you feel the space is wild and noisy, that is normal. It actually is.

Why people care about cryptocurrencies

People are drawn to crypto for different reasons. You might see yourself in one of these.

- Speculation and potential high returns A lot of people are here because they see big upside. Crypto has had insane bull runs. The flip side is brutal drawdowns, which we will talk about later.

- Portfolio diversification If you already own stocks, bonds, property, you might see crypto as a new asset class, especially “digital gold” narratives around Bitcoin.

- Censorship-resistant payments In countries with capital controls, sanctions, or unstable banking systems, using crypto or stablecoins can sometimes be the only way to move money. It is not perfect, but it is a real use case.

- Innovation in finance and tech Developers and investors see DeFi, Web3, NFTs and tokenized real-world assets as a new financial and internet layer. If you like being early in new tech, this is part of the appeal.

If you are just curious and not sure where you fit yet, that is fine. Reading a straightforward guide like this is exactly the right first step.

How cryptocurrencies work, in simple terms

You do not need to be a programmer to understand the basics. Let me walk you through the moving parts like I would with a friend over coffee.

Blockchain in simple terms

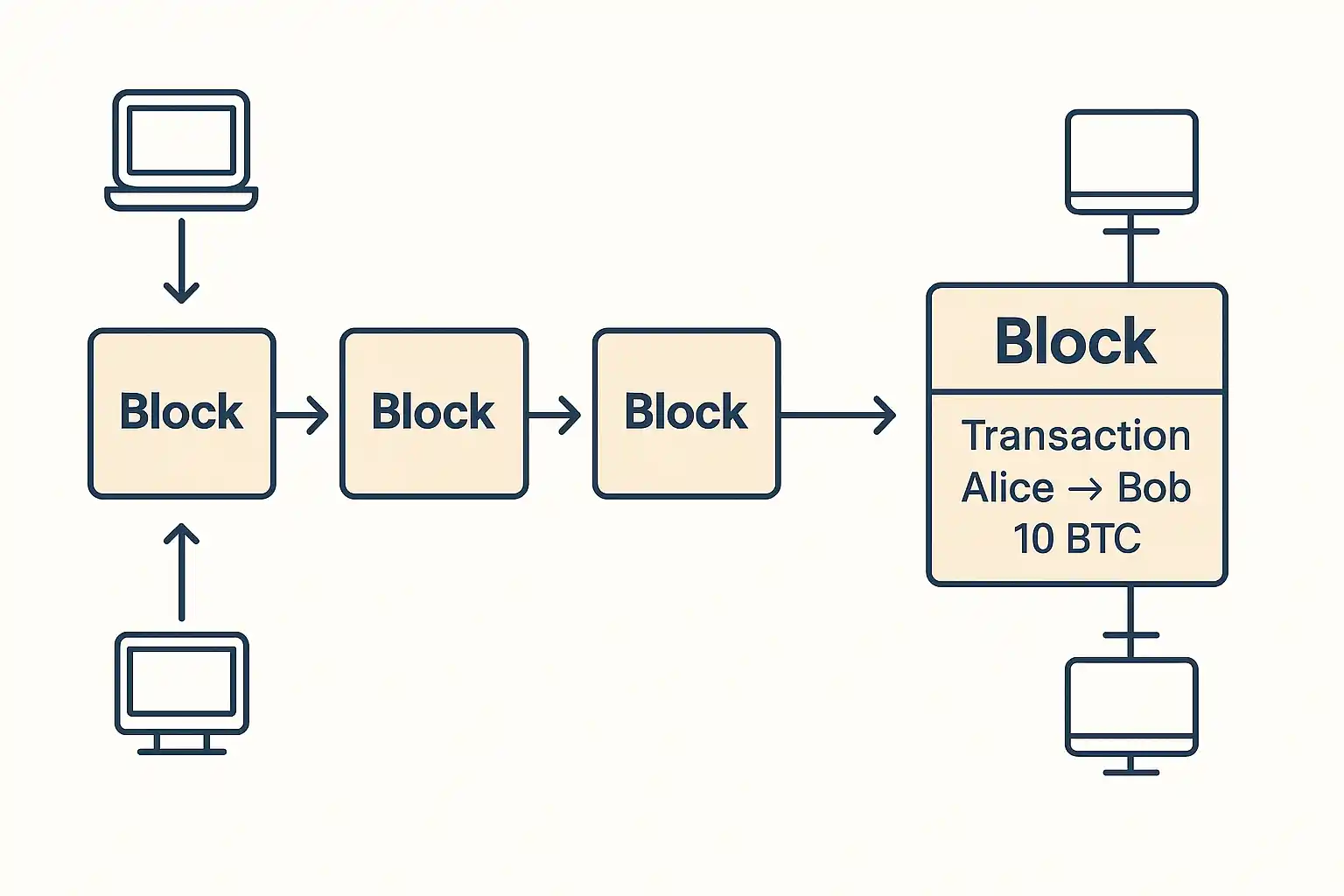

Imagine a notebook where every page lists recent transactions. Once the page is full, you seal it, number it, and glue it to the back of the notebook. You never rip pages out.

That notebook is the blockchain. Each page is a block.

Now imagine instead of one notebook, thousands of people around the world all keep a copy. Every time a new page is added, they all agree on what is written, then they all glue the same page into their notebook.

That is roughly how a blockchain works.

This design gives you some nice properties:

- Transparency , anyone can see transactions on most public chains

- Tamper-resistance because changing old data would require rewriting a huge amount of history on many computers

- No single point of failure because there is no central server to shut down

Public and private keys, wallets and addresses

This part is absolutely critical for you as an investor. This is where people either stay safe or get wrecked.

When you use crypto, you have:

- A public address , which is like an email address where people can send you coins

- A private key or seed phrase , which is like the master password that proves you own and can move those coins

A wallet is just software or hardware that stores and uses these keys.

There are a few main types:

- Custodial wallets , for example on exchanges, where the platform controls the keys and you just see a balance

- Non-custodial software wallets , mobile or desktop, where you hold the seed phrase

- Hardware wallets , small physical devices that keep your private keys offline

Here is the bottom line. Whoever controls the private key controls the coins. If you lose your seed phrase, or someone else gets it, that money is gone. No “forgot password” button.

A simple Bitcoin transaction

Let's say Alice wants to send Bitcoin to Bob. When you click “send” on an exchange, this is roughly what happens in the background.

- Alice's wallet creates a transaction saying “I want to send X BTC from my address to Bob's address”

- That transaction is broadcast to the Bitcoin network

- Miners or validators bundle many transactions into a block

- The network agrees which block is valid and adds it to the chain

- After a few more blocks, the transaction is considered final and hard to reverse

You do not see all this when you use an app. You just see “pending” then “confirmed”. But under the hood, this process is what gives you a system that does not rely on a single bank or payment processor.

Consensus mechanisms, how the network agrees

Different blockchains use different methods to decide which transactions are valid and who gets to write the next block. Two big ones you will hear about are:

Proof of Work (PoW) This is what Bitcoin uses. Miners compete by doing intense calculations with hardware. The first miner to solve the puzzle gets to add the block and receives a reward.

Pros, it is battle tested and secure if enough computing power is involved. Cons, it uses a lot of energy and is slower than many newer designs.

Proof of Stake (PoS) Here, validators lock up, or “stake”, their coins. The protocol chooses validators to propose and validate blocks, often in proportion to how much they have staked, with some randomness.

Pros, much lower energy use and often faster confirmation times. Cons, different trade-offs around centralisation and incentives.

Ethereum switched from PoW to PoS, which massively cut its energy usage.

Scalability, Layer 1 vs Layer 2

You might have noticed, when markets are crazy, Ethereum fees spike and network congestion kicks in. That is the scalability problem.

- Layer 1 is the main blockchain, like Bitcoin or Ethereum

- Layer 2 solutions sit on top, they process lots of transactions off the main chain, then post a summary back

Examples include rollups and sidechains. The goal is simple, keep the security of the main chain, but make everyday transactions faster and cheaper.

If you are a trader, this matters because it affects your fees, the speed of your trades, and which platforms you choose to use.

Types of cryptocurrencies

Not all coins are trying to do the same thing. Treating them all the same is a fast way to misjudge risk.

Payment coins, “digital cash” and “digital gold”

These are the older style coins like Bitcoin and Litecoin that were originally pitched as money.

Bitcoin has a fixed supply cap of 21 million coins. That scarcity is why some people see it as “digital gold”. In practice, most people use it more as a store of value or speculative asset, not day-to-day spending money.

As a medium of exchange, it is accepted in some online stores and in specific countries, but it is still niche compared to normal payments. As a store of value, its long term trend is up, but the path involves heavy crashes. If you are a beginner, you need to be comfortable seeing deep drawdowns.

Smart contract and platform tokens

These are coins like ETH, SOL, BNB, AVAX and others, which power blockchains that host applications.

Developers build decentralised exchanges, lending markets, NFT marketplaces, games, and a lot more on these chains. To use those apps, you pay fees in the native coin.

If you are looking at these as investments, you are not just betting on the coin, you are betting on the entire ecosystem of apps and users that might grow on that chain.

Stablecoins

Stablecoins aim to keep a stable price, usually 1 USD per token. They are the “cash” leg of the crypto ecosystem.

You will see a few models:

- Fiat-backed stablecoins like USDT or USDC, where each coin is supposed to be backed by dollars or safe assets such as short-term US Treasuries

- Crypto-backed stablecoins like DAI, where you lock up more volatile crypto as collateral

- Algorithmic stablecoins , which rely on smart contract mechanisms rather than full reserves, and have a history of blowing up

The big regulatory milestone here is the GENIUS Act in the US, which is a federal law that creates a full framework for payment stablecoins, including strict reserve rules and supervision. If you want to see how serious that is, you can look at the official bill text on Congress.gov .

For you, the main takeaway is simple. Stablecoins are useful for trading and cross-border movement of money, but they are not risk free. You are trusting the issuer and the legal framework around them. De-pegs do happen.

Utility and governance tokens

Many DeFi protocols and Web3 projects issue tokens that:

- Give you discounts or access to services

- Let you vote on protocol settings and treasury decisions

These can look like “shares of a decentralised company”, but legally it is more complicated. In some jurisdictions, certain tokens may be treated as securities. That has big implications for regulation and investor protection. If you are trading them, understand you are in a more complex grey area.

Security tokens and tokenized real-world assets (RWA)

Here we move into the overlap between traditional finance and crypto.

Security tokens and RWA tokens represent things like:

- Government bonds

- Money market funds

- Real estate shares

- Private credit

The idea is, you can buy a token that represents a real financial asset, sometimes in smaller chunks, and sometimes with 24/7 trading on chain. There is real institutional interest here.

If you are a more advanced investor, you will see talk of RWA yields, tokenized Treasuries, on-chain funds. Just remember, the token is only as good as the legal structure and the entity behind it. This is still early and evolving.

Memecoins and highly speculative tokens

Dogecoin, Shiba Inu, and the latest meme of the week, all sit in this bucket.

They are driven mainly by community, jokes, and hype. Sometimes they produce huge short term gains. Sometimes they go to zero after a brief pump. Fundamentals are often thin or non-existent.

If you play in this area, treat it like high risk punting. Money you can afford to lose, not rent money, not your emergency fund.

Cryptocurrencies vs money, CBDCs and tokenized deposits

A good way to ground yourself is to go back to the boring textbook definition of money.

Do cryptocurrencies function as money?

Economists usually say money has three main functions:

- Medium of exchange

- Unit of account

- Store of value

Most cryptocurrencies are weak in at least two of these today.

As a medium of exchange , you can spend crypto at some merchants and for specific online services, and stablecoins are useful in some countries for remittances and cross-border payments. But compared to cards and bank transfers, usage is still small.

As a unit of account , almost everything in your life is still priced in fiat, like dollars, euros, pounds. You do not get your salary in “0.002 BTC” or see your rent in “0.8 ETH” in most of the world.

As a store of value , Bitcoin and a few others have done well over long enough timeframes, but you need the stomach for swings of 50 to 80 percent in bear markets. That is not a “safe” store of value in the traditional sense.

So, in real life, most cryptocurrencies behave more like speculative assets than traditional money.

Cryptocurrencies vs fiat currency

Fiat currency, like USD or EUR, is:

- Issued by a central bank

- Backed by government and legal tender laws

- Managed through monetary policy, interest rates, and banking rules

Cryptos are:

- Not legal tender in most countries

- Not backed by a central bank

- Valued purely by what buyers and sellers are willing to pay on the market

Stablecoins are a partial bridge here, but you are still exposed to issuer risk and regulatory risk.

CBDCs, central bank digital currencies

CBDCs are digital versions of central bank money. Think of them as “digital cash” issued directly by the central bank.

Key differences from crypto:

- CBDCs are state-backed and centralised

- They can be designed to be interest bearing or not

- Governments control the rules, privacy, and access

In practice, CBDCs could coexist with crypto and stablecoins, or they could compete with them, depending on how they are designed and regulated. As an investor, CBDCs are more of a macro theme than a direct trading instrument, at least for now.

Tokenized bank deposits and other regulated digital assets

Banks are also exploring tokenized deposits. This is where your ordinary bank money is represented as a token on a permissioned blockchain.

The promise is simple. You keep the protections of regulated bank money, but you get some of the speed and programmability of blockchain rails.

For you, the key thing is to recognise that “digital assets” is becoming a broad category. Crypto is not just Bitcoin any more.

Crypto market structure and how to invest

Now let's get into the part you probably care about most. How do you actually get exposure, and what should you watch out for.

Where and how crypto is traded

You will mostly interact with crypto in three places:

Centralised exchanges (CEX) These are platforms like Binance, Coinbase , Kraken and others. You sign up, pass KYC checks, deposit fiat or crypto, and trade via an order book.

Pros, deep liquidity in major pairs, familiar trading interface, fiat on-ramps. Cons, you rely on the exchange's security and solvency. We have seen big failures in the past.

Decentralised exchanges (DEX) DEXs like Uniswap or Curve run as smart contracts on blockchains. You connect a wallet and trade directly from your own address.

They often use automated market makers (AMMs) rather than traditional order books. This is a different mechanism, but the end result is the same for you, you swap one token for another.

Pros, you keep control of your funds, no central custodian. Cons, smart contract risk, sometimes worse slippage, sometimes fake tokens.

Brokers and fintech apps Apps like Revolut, Robinhood, PayPal and similar let you buy and sell crypto inside a broader finance app.

They tend to be beginner friendly on the surface. The trade off is, sometimes you cannot withdraw coins to your own wallet, or the range of assets is limited.

As a rule of thumb, if you are going beyond basic exposure, you will want the ability to withdraw to your own wallet sooner or later.

How to buy your first cryptocurrency

If you are a beginner, a simple process keeps you out of most trouble:

- Pick a reputable platform, ideally one that is regulated in your country or region

- Open an account and complete verification

- Turn on strong security, use a unique password and app based two factor authentication

- Deposit a small amount of fiat using a method with sensible fees

- Place a basic order, start with a liquid coin like BTC or ETH

- Once you are comfortable, learn how to withdraw to a personal wallet if you plan to hold longer term

Custody and storage basics

You have two big choices for storing your coins:

- Leave them on the exchange

- Move them to your own wallet

Leaving coins on a major exchange is convenient, especially if you trade often. But you are exposed to exchange hacks, insolvency, and legal issues.

Self custody gives you control, but now you are your own bank. You must secure your devices, back up your seed phrase, and protect yourself from scams. For significant amounts, a good hardware wallet plus an offline backup of your seed phrase is standard practice among serious investors.

If you are new, you can start on an exchange while you learn, then move into self custody as your knowledge and position size grows.

Core trading concepts for new traders

Crypto markets do not sleep. They trade 24/7, 365 days a year. That is fun at first and exhausting later.

A few things you should understand early:

- Liquidity , how easy it is to buy or sell without moving the price too much

- Spread , the gap between the best buy and sell prices

- Slippage , the difference between the price you expect to trade at and the price you actually get, especially in fast markets

- Order types , market orders fill immediately at the best available price, limit orders wait for your chosen price, stop orders trigger entries or exits when a level is hit

For most beginners, simple spot trades with limit and market orders are enough. Futures, perpetual swaps and options can be powerful, but they also bring leverage and liquidation risk. Respect them.

Investment vehicles beyond just holding coins

You do not have to hold coins directly to get crypto exposure. You also have:

- Spot purchases on exchanges

- Crypto ETFs and ETPs, for example spot Bitcoin ETFs that were approved in major markets in 2024 and beyond

- Listed companies that earn a large share of profits from crypto, exchanges, miners, stablecoin issuers, and so on

- Trusts and closed-end funds that hold coins on your behalf

The trade offs usually revolve around fees, custody, and convenience. If you are not comfortable with self custody, an ETF might be easier, but you pay ongoing management fees.

Staking, yield and DeFi income

This is where a lot of people chase returns and get hurt. So let's go carefully.

On proof-of-stake chains, you can stake your coins, either directly or via a service, and earn rewards for helping secure the network.

In DeFi, you might:

- Lend coins into a lending protocol and earn interest

- Provide liquidity to a DEX and earn trading fees and token incentives

- Use structured products that bundle strategies together

All of this sounds great when yields are high. The risks are real:

- Smart contract bugs and exploits

- Protocols collapsing

- Peg breaks in stablecoins

- Regulatory changes that make some products much harder to offer

After the GENIUS Act in the US, we are likely to see more clarity around interest-bearing stablecoin products, but that does not remove protocol risk.

If you are just starting out, focus on understanding spot markets first. Treat yield products as advanced tools, not free money.

How much to allocate, portfolio thinking

This part is personal, but there are a few principles that serve most people well.

- Do not use money you need for rent, food, or essential bills

- Keep crypto as a small slice of a broader portfolio at first, think single digit percentages, not everything you own

- Expect big drawdowns and plan around them

- Be honest about your own temperament, if a 50 percent drop will make you panic sell, size your position smaller

Crypto can be an interesting part of a diversified portfolio, but only if you treat it like an investment, not a lottery ticket.

Real-world use cases and potential benefits

Despite all the noise, there are real use cases. They might not match the hype, but they are not nothing.

Cross-border payments and remittances

If you have ever tried to send money overseas using a bank, you know the pain. High fees, slow settlement, horrible FX spreads.

Stablecoins give you a different option. You can send value directly to someone's wallet in minutes. They might then cash out locally, or keep it in stablecoins if their local currency is weak.

In some countries with capital controls or hyperinflation, this is not theory, it is daily life.

Decentralised finance (DeFi)

DeFi is about rebuilding financial services on open blockchains.

You have decentralised exchanges, lending and borrowing markets, synthetic assets, and yield strategies. Everything runs through smart contracts instead of traditional intermediaries.

Benefits include open access, transparent on-chain data, and programmable money. The flip side is smart contract risk, governance failures, and some fragile designs.

If you want to see how mainstream financial bodies are thinking about this, organisations like the World Economic Forum publish analysis on DeFi and financial inclusion on weforum.org .

NFTs and digital collectibles

NFTs are tokens that represent unique items. In 2021 it was all about profile pictures and speculative art. Then the bubble cooled down.

The more interesting part long term is:

- Game items

- Ticketing

- Loyalty programs

- Digital identity and credentials

For you as an investor, NFTs are high risk and illiquid. They are more like early stage art or collectibles than traditional investments.

Before you buy, run a structured pricing checklist from Valuing NFTs Basics so rarity, liquidity, and community strength are evaluated together.

Web3, DAOs and decentralised governance

Web3 is the idea of an internet where you own more of your data, identity and value.

DAOs, decentralised autonomous organisations, are token-governed groups where holders vote on decisions and spending. Some manage billions in assets, others are small and experimental.

This area is exciting, but young. Governance capture, apathy, and regulatory uncertainty are all real problems.

Tokenization of real-world assets

We touched on this earlier. Tokenizing bonds, funds, property and credit is attractive to both traditional finance and DeFi.

The pitch is clear. You get fractional ownership, faster settlement, 24/7 markets, and the ability to plug those assets into DeFi protocols.

The questions are also clear. How do you handle regulation, investor protection, and the boring operational stuff. Over time, this could become one of the biggest uses of blockchain tech.

Enterprise and institutional use cases

Banks and large companies are not blind to all this.

You see experiments and real projects in:

- Cross-border payments

- Collateral management

- Trade finance

- Treasury management using tokenized deposits and stablecoins

Payment networks like Visa and PayPal are also integrating stablecoin support. This is not the cool Twitter side of crypto, but it is worth watching if you care about long term adoption.

Risks, security and how to protect yourself

This is the section I wish more people read before buying anything. If you only skim one part, let it be this one.

Market risks

Crypto is volatile. That is not a cute disclaimer, it is reality.

- Coins can drop 50 percent in a few weeks

- Altcoins can go down 90 percent or more and never recover

- Correlation with “risk on” assets like tech stocks can spike during macro stress

If you are emotionally or financially unable to handle those swings, size your exposure accordingly. There is no shame in deciding the space is not for you.

Liquidity and slippage

Big coins like BTC and ETH are usually liquid on major exchanges. Smaller tokens are not.

In low liquidity coins:

- A relatively small market order can move the price a lot

- During crashes, bids can vanish and spreads can widen

- Exiting a large position can be painful or impossible without heavy slippage

If you are trading small caps, always look at volume and depth, not just price.

Technology and cybersecurity risks

The tech stack here is complex. There are plenty of attack surfaces:

- Protocol bugs in smart contracts

- Oracle failures that feed bad data into DeFi systems

- Exchange hacks and insider theft

- Wallet malware, fake wallet apps, keyloggers, and SIM swap attacks on your phone

As a user, you cannot fix protocol code, but you can choose to use battle tested platforms, avoid chasing every new farm, and secure your own devices properly.

Operational and counterparty risks

This is where names like FTX come in.

If you keep assets on a centralised platform, you are exposed to:

- Mismanagement or outright fraud

- Poor risk controls

- Legal fights in bankruptcy that might lock your funds for years

Centralised lenders and yield platforms have also gone under after taking too much risk with user deposits. On paper things looked safe, until they were not.

And then there is the simple but brutal operational risk of self custody. If you lose your seed phrase or send coins to the wrong address, it is usually irreversible.

Scams and fraud types you will actually see

Unfortunately, crypto is full of people trying to separate you from your money. Common patterns include:

- Ponzi schemes dressed up as “investment programs” with fixed daily returns

- Rug pulls, where token creators disappear with liquidity

- Fake exchanges and phishing sites that mimic real brands

- Wallet drainer links hidden in fake airdrops or NFT mints

- Romance scams and fake celebrity or influencer endorsements

Again, the Kaspersky guide I mentioned earlier has a decent breakdown of common scam structures and what they look like in practice. Combine that with a healthy dose of scepticism and you avoid most traps. The most dangerous variant in 2026 is the malicious token-approval signature - a single careless signature on the wrong site can drain every asset in the connected wallet in one transaction. Our approval phishing protection playbook walks through how to spot drainer sites, how to revoke stale allowances, and the browser-wallet settings that actually block these scams before they hit.

Security hygiene, practical habits

A few boring, unsexy habits make a huge difference:

- Use hardware wallets for serious amounts

- Turn on app based 2FA, avoid SMS where possible

- Never type your seed phrase into a website or share it with anyone, ever

- Bookmark official URLs and use those, not links from DMs

- Keep your phone and computer updated and protected with decent security software

Think about yourself like a small digital bank. If a bank behaved the way many people behave online, you would never trust it.

Investment risk management

Even if you get the tech and security right, you can still blow up your account with bad risk management.

Simple guidelines:

- Only invest what you can afford to lose without wrecking your life

- Keep crypto as a proportion of a broader portfolio, not your only asset

- Do not over concentrate in illiquid small projects

- Be careful with leverage, especially in perpetual futures, liquidation can wipe you out in seconds

For active trading, the position size calculator and the risk of ruin calculator help quantify exposure before you click.

You will still make mistakes, everyone does, but this keeps the damage survivable.

Global regulation and tax, what new investors should know

You do not need to be a lawyer, but ignoring regulation is a good way to get surprised later.

Why regulation matters

Regulation affects:

- Which exchanges can operate in your country

- Whether you can legally trade certain products

- How safe or risky a given platform is

- How your profits are taxed

It also shapes whether big institutions feel comfortable entering the space, which feeds back into liquidity and long term adoption.

Common regulatory themes

Across most major regions, you see similar goals:

- KYC and anti-money-laundering rules for exchanges and service providers

- Travel rule requirements for larger transactions

- Debate over whether certain tokens are securities, commodities, or something else

The details differ, but the direction is clear. The “wild west” era is slowly narrowing, especially around stablecoins and large platforms.

United States

In the US:

- Many crypto exchanges are treated as money service businesses and must follow strict AML rules

- IRS treats crypto as property, meaning disposals trigger capital gains or losses, whether you sell for cash or spend crypto directly

The big new piece of legislation is the GENIUS Act, which sets out a full regulatory framework for payment stablecoins, including reserve requirements and oversight. That is a major change for the stablecoin segment and for payment-focused use cases.

On the investment side, approval of spot Bitcoin ETFs has also brought more traditional capital into the space and given conservative investors another way to get exposure.

European Union

The EU's MiCA regulation creates a unified framework for:

- Licensing crypto service providers

- Setting rules on stablecoin reserves, disclosures, and governance

- Defining different classes of tokens

For you as an EU user, this should eventually mean more consistent protections and less “regulatory shopping” by shady platforms.

United Kingdom

The UK is folding crypto more tightly into its existing financial regime. That includes:

- Rules on marketing and promotions

- Oversight of custody and exchange services

- Work on regulating stablecoins as potential payment instruments under existing e-money style laws

The tone is “cautious but open”, rather than a blanket ban.

Other key hubs

Some other important regions:

- Singapore , licensing under the Payment Services Act with strong investor protection focus

- Dubai (VARA) , a dedicated crypto regulator attracting many exchanges

- Hong Kong , reopening to regulated retail crypto trading through licensed platforms

At the same time, a few countries still have strict bans or heavy restrictions. Always check your local rules before getting involved.

Tax basics

This will not be tax advice, but you should understand the general pattern. In many countries:

- Trading profits are treated as capital gains

- Spending crypto on goods or services is a taxable disposal event

- Mining, staking, and airdrop rewards can be taxed as income when you receive them, then capital gains apply if you later sell at a different price

The one habit I strongly recommend is keeping good records from day one. Every trade, every transfer, every reward. Tax authorities are catching up, and exchanges increasingly share data.

If your positions are meaningful, talk to a local tax professional who understands crypto. It is cheaper than getting it wrong.

The future of cryptocurrencies, trends and open questions

Let's zoom out for a moment. Where might all this be heading, and what should you keep an eye on as a trader or investor.

Institutional adoption and RWAs

Institutional interest is growing, slowly and unevenly, but it is real.

- Crypto ETFs and ETPs are expanding

- More funds are adding small allocations to digital assets

- Tokenization of real-world assets is moving from slide decks to live products

If you care about long term value, watch where real balance sheet money is moving, not just social media hype.

Integration with traditional finance

The lines between “crypto” and “traditional finance” are blurring.

We are seeing:

- Stablecoins integrated into global payment networks

- Banks building internal settlement systems on blockchain rails

- Joint ventures between big finance and crypto native firms

In the long run, you may stop thinking “on chain vs off chain” and just see a spectrum of digital assets with different regulatory wrappers.

Technological evolutions

Under the surface, a lot of engineering work is happening on:

- Better smart contract security and formal verification

- Smart wallets where you can recover access without giving a company full control

- Account abstraction, which can hide some of the complexity from users

- AI agents that can hold and move funds on chain under rules you define

You do not need to understand all the details, but stay alert to how UX is improving. The easier safe usage becomes, the more mainstream adoption you are likely to see.

ESG and sustainability debates

Proof of Work chains like Bitcoin are often criticised for energy use. Supporters argue about renewable mixes and security benefits.

Proof of Stake and newer designs reduce energy use a lot. Green mining and location-based solutions are also part of the story.

If you run money for clients or care deeply about ESG, this debate is worth following, because it affects which assets institutions are allowed to hold.

Financial inclusion vs speculation

Crypto supporters often highlight:

- Access to dollar-linked stablecoins in unstable economies

- Open access financial tools without needing a bank account

- Protection against censorship and capital controls

Sceptics point to:

- Bubbles and crashes

- Scams and rug pulls

- Lack of intrinsic cash flows for many tokens

Both sides have valid points. Your job as an investor is not to join a tribe, it is to look at where real, sustainable value is being created, and price in the risks honestly.

Big open questions

No one knows the answers yet, but these are the questions that will shape the next decade:

- Will global regulation converge enough to make cross-border compliance workable

- How will major bans, such as in some large economies, influence adoption and innovation

- Will we see a true “killer app” in Web3, like a social network, game, or identity system that brings in hundreds of millions of normal users

- Will people still say “crypto” in ten years, or will we just talk about different types of digital assets, including CBDCs and tokenized everything

As a trader or investor, these are the themes you want to keep an eye on, even if your day to day focus is short term price moves.

Is crypto right for you, a quick self-check

Before you open that app and fund an account, it is worth asking yourself a few honest questions.

- What is my time horizon, am I thinking in weeks, months, or years

- How would I feel if my crypto holdings dropped 80 percent

- Do I actually understand what I am buying, or am I following someone else blindly

- Am I already diversified in safer assets like cash, bonds, and broad equity funds

If you are a beginner, a simple starting point is a small, diversified allocation into large, liquid coins like BTC and ETH, with no leverage.

Use that period to learn, read more detailed guides, and get comfortable with wallets and security. As your knowledge and confidence grow, you can decide whether to increase exposure or keep it small.

There is no prize for being all in. Surviving long enough to learn and adapt is the real win.

Frequently asked questions

Here are some short, straight answers to the questions I get all the time.

What is a cryptocurrency in simple terms? It is digital money that lives on a blockchain. Instead of a bank updating a ledger, a network of computers does it together using cryptography.

How do cryptocurrencies gain value? Mainly through supply and demand. If more people want to hold or use a coin than sell it, price goes up. In some cases there are cash flows or real world backing, in many cases there are not.

How is cryptocurrency different from traditional money? Traditional money is issued by governments and central banks, and is legal tender in your country. Crypto is not, in most places, and is not backed by a government. Its value is market based.

Is cryptocurrency safe for beginners? The tech can be used safely, but the market is risky. If you are a beginner, start small, focus on the top assets, secure your accounts properly, and never invest money you cannot afford to lose.

How much should I invest in cryptocurrency? There is no magic number. Many cautious investors start with a low single digit percentage of their total investable assets, then adjust over time as they learn and see how they handle volatility.

What are the most popular cryptocurrencies right now? Bitcoin and Ethereum remain the two largest by market value. After that, the list changes more often, but you will usually see other major platform tokens and large stablecoins.

What is the difference between Bitcoin and Ethereum? Bitcoin is mainly focused on being a store of value and sound money with a fixed supply. Ethereum is a programmable platform where you can build apps, and ETH is the fuel that powers those apps.

What is the difference between cryptocurrency and blockchain? Blockchain is the underlying technology, a way of recording data. Cryptocurrency is one use of blockchain, where the data recorded is ownership and transfers of digital assets.

Can cryptocurrencies be banned or shut down? Governments can ban exchanges and make usage illegal locally, which makes access harder. It is much harder to “shut down” a large, decentralised network globally, but local regulation still matters a lot for you as a user.

Are cryptocurrencies anonymous? Most major chains are pseudonymous. Addresses are not tied to your real name on chain, but transactions are public, and links can often be made using exchange data and other clues. Privacy coins and tools exist, but they come with their own risks.

How do I keep my cryptocurrency safe? Use strong security on accounts, enable 2FA, store significant holdings in a hardware wallet, back up your seed phrase offline, and avoid clicking random links or connecting your wallet to unknown websites.

What happens if my exchange is hacked or goes bankrupt? You may lose some or all of your funds, depending on how the platform is structured and what happens in legal proceedings. This is why many experienced users avoid keeping large balances on centralised platforms.

How do stablecoins stay pegged to the dollar? Fiat-backed stablecoins aim to keep 1:1 reserves in cash and short term safe assets, and allow redemptions. Market makers help keep the price at or near one dollar. Algorithmic designs try more complex mechanisms and have a mixed history.

What is tokenization of real-world assets? It is when you represent ownership of a real asset, like a bond or property share, with a token on a blockchain. That token can then be transferred and used in digital markets.

Do I have to pay taxes on crypto profits? In most countries, yes. Profits from trading or investing are usually taxable, and in many places spending crypto is also a taxable event. Check your local rules.

Can I convert crypto back into cash easily? On major exchanges with proper banking access, converting into fiat is usually straightforward, subject to KYC and withdrawal limits. In restrictive jurisdictions, it can be harder.

What are gas fees and why are they sometimes high? Gas fees are payments to the network for processing your transaction. When a chain is busy, users bid higher fees to get included faster, which pushes average fees up.

What is DeFi, decentralised finance? It is a set of financial services built on blockchains using smart contracts, things like trading, lending, and derivatives without traditional intermediaries.

What is an NFT? A non-fungible token, a unique digital token that usually represents an item like art, a game asset, or a ticket.

Will cryptocurrencies replace banks? More likely, they will push banks and regulators to adapt. You may see a hybrid world where traditional institutions, stablecoins, and public blockchains all coexist.

Is crypto a good hedge against inflation? Sometimes, sometimes not. Over certain periods, assets like Bitcoin have done well when fiat concerns rise, but in other periods they trade more like high risk tech stocks. Treat the “inflation hedge” idea as a narrative to test, not a guarantee.

Glossary, quick reference

A few short definitions you can come back to when you forget a term, which is normal.

Blockchain A shared, append-only database where transactions are grouped into blocks and linked together using cryptography.

Wallet Software or hardware that stores your private keys and lets you send and receive crypto. Hot wallets are always online, cold wallets keep keys offline.

Public key / address The identifier you share with others so they can send you funds.

Private key / seed phrase The secret that proves you own your funds. Anyone who has it can spend your coins.

Consensus The process by which a blockchain network agrees on the valid state of the ledger.

Proof of Work / Proof of Stake Two major consensus methods. PoW uses computing power and energy, PoS uses staked coins.

Stablecoin A token that aims to keep a stable value, usually pegged to a fiat currency like the US dollar.

Smart contract Code that runs on a blockchain and automatically executes rules when conditions are met.

DeFi Decentralised finance, financial services built using smart contracts instead of traditional intermediaries.

NFT Non-fungible token, a token that represents a unique item rather than an interchangeable unit.

DAO Decentralised autonomous organisation, a group coordinated via smart contracts and token based voting.

RWA Real-world asset, a token that represents something like a bond, fund, property, or other off-chain asset.

KYC / AML Know Your Customer and Anti-Money-Laundering, regulatory requirements around identity and crime prevention.

Gas fee The fee you pay to have your transaction processed on a blockchain.

Slippage The difference between the price you expect to trade at and the price you actually get.